What the Inflation Reduction Act Did for Commercial Solar

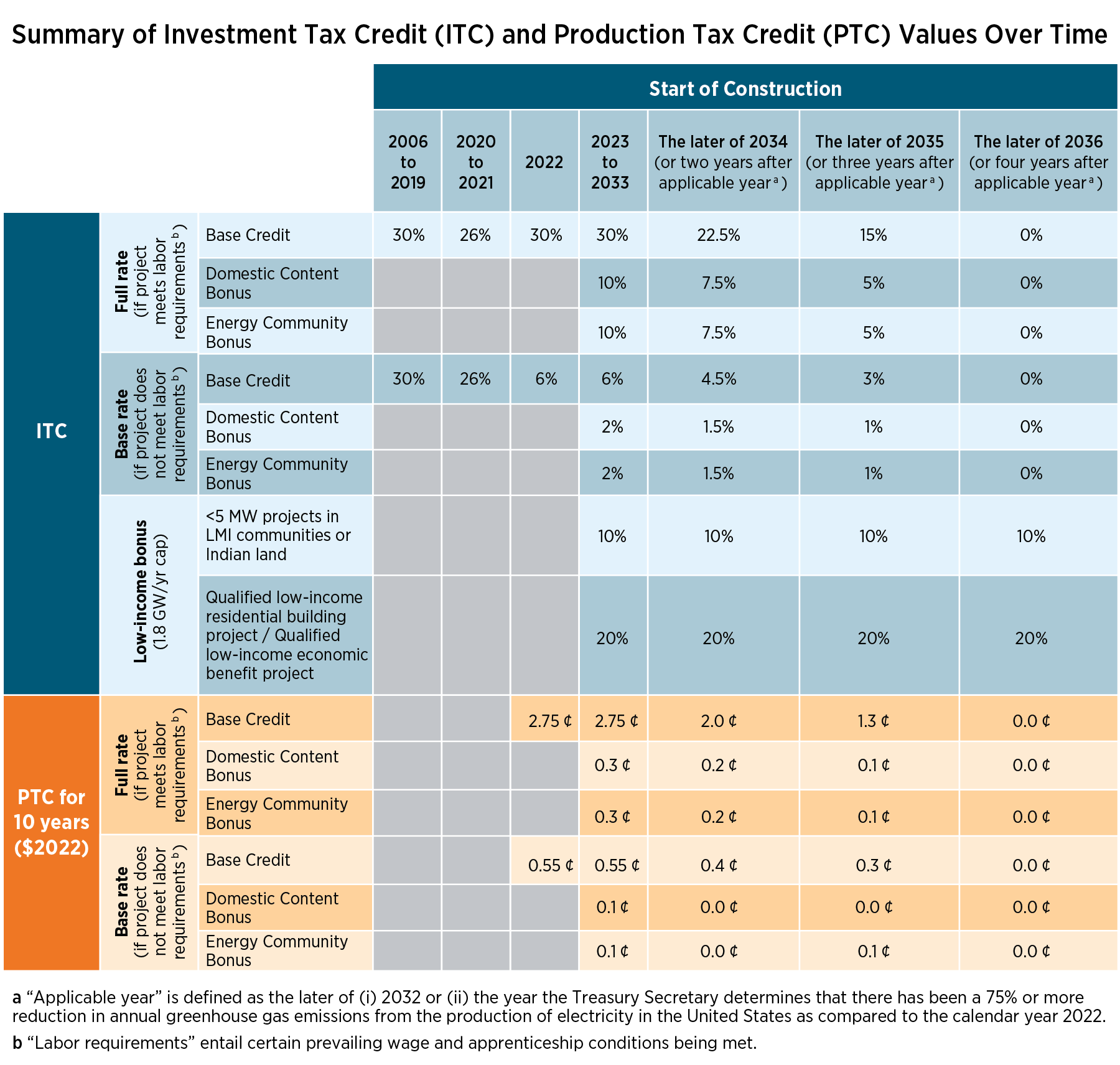

The Inflation Reduction Act, signed in August 2022, created the most significant expansion of commercial solar tax incentives in US history. It replaced the old Section 48 ITC with the new Section 48E Clean Electricity Investment Tax Credit, extended the 30% base credit through 2032 (previously it was scheduled to step down), and added a suite of stackable bonus credits that can push the total ITC to 50% or higher for qualifying projects.

The key IRA provisions for commercial solar were: a 30% base ITC for all qualifying commercial solar systems placed in service by December 31, 2032; a 10% energy community adder for projects in census tracts with historical fossil fuel employment or brownfield sites; a 10% domestic content adder for systems meeting IRS-specified domestic manufacturing thresholds; a 10% low-income community adder for qualifying projects in designated areas; and the Section 6417 Direct Pay provision allowing nonprofits and government entities to receive ITC value as a direct cash payment rather than a tax credit.

What the One Big Beautiful Bill Act Changed

The One Big Beautiful Bill Act (OBBBA), signed by President Trump on July 4, 2025, modified the IRA solar credits significantly. Understanding what changed — and what didn't — is essential for any commercial solar project starting in 2025 or 2026.

What the OBBBA changed: it moved the ITC placed-in-service deadline from December 31, 2032 to December 31, 2027, effectively compressing the remaining window for new commercial solar projects by five years. It established a construction start safe harbor deadline of July 4, 2026 — projects that began construction (as defined by the IRS physical work test or 5% safe harbor) by that date retain the full ITC eligibility regardless of when they are placed in service. It also added FEOC restrictions (Foreign Entity of Concern) that deny the domestic content adder for systems using solar panels or components from Chinese, Russian, Iranian, or North Korean manufacturers for projects starting construction after July 4, 2025.

What the OBBBA did not change: the 30% base ITC remains intact for projects placed in service by December 31, 2027. The energy community adder (10%) remains available and is not affected by FEOC rules. The Direct Pay provision for nonprofits remains intact. The MACRS 5-year depreciation schedule is unchanged. Full OBBBA bill text is available via Congress.gov.

Where Things Stand in July 2026

As of today, the July 4, 2026 construction start safe harbor deadline has passed. This means new commercial solar projects beginning construction now cannot use the safe harbor to protect ITC eligibility — they must be placed in service (system commissioned and grid-connected) by December 31, 2027 to claim the ITC. With typical Illinois commercial solar projects running 5-8 months from signed contract to commissioning, and with interconnection timelines for downstate Illinois and other states running 90-150 days, projects starting in mid-2026 face a tight but achievable 2027 timeline.

The most important action for any business considering commercial solar right now is to begin the proposal and interconnection process immediately. Interconnection queue positions are first-come, first-served at most utilities — filing early protects your timeline. See our due diligence checklist for the questions to ask before signing, and our 2026 deadline blog post for a full timeline analysis.

The FEOC Restriction: What It Means for Equipment Sourcing

The FEOC (Foreign Entity of Concern) restriction introduced by the OBBBA affects the domestic content adder (worth 10% on top of the 30% base ITC) for projects beginning construction after July 4, 2025. A project cannot claim the domestic content adder if it uses solar panels, inverters, or mounting systems manufactured by companies with significant ownership ties to China, Russia, Iran, or North Korea.

This does not affect the 30% base ITC or the energy community adder. It only affects the 10% domestic content bonus. In practical terms, most commercial solar projects using US-manufactured panels from companies like First Solar, Silfab, or QCells (US facilities) qualify for the domestic content adder and are not subject to FEOC restrictions. Projects using panels from Chinese-owned manufacturers — regardless of where they are physically assembled — may lose the domestic content bonus but retain full 30% base ITC eligibility.

Our team verifies FEOC compliance for every project as a standard step in equipment specification. For further guidance, the IRS published Notice 2023-29 and subsequent updates covering domestic content documentation requirements.

Nonprofits and Tax-Exempt Entities: Direct Pay

The IRA's Section 6417 Direct Pay provision, which survived the OBBBA unchanged, allows eligible tax-exempt entities — including 501(c)(3) nonprofits, government agencies, tribal governments, rural cooperatives, and others — to receive the value of the ITC as a direct cash payment from the Treasury rather than a tax credit offset. This means a qualifying nonprofit can receive a check equal to 30-50% of system cost in the year the system is placed in service, effectively providing the same financial benefit as the ITC without requiring federal tax liability.

Direct Pay is filed with the organization's annual tax return using IRS Form 3468 and an elective payment election. Our team works with nonprofit solar candidates through the full process. See our nonprofit solar page for a complete guide, including Direct Pay eligibility requirements and application timing.

Stacking ITC Credits: The Full Calculation

For qualifying commercial solar projects in 2026, the full ITC calculation looks like this. The base credit under Section 48E is 30% of eligible project cost for systems placed in service before December 31, 2027. Projects in qualifying energy community census tracts — use the DOE Energy Communities mapping tool — add 10 percentage points, bringing the credit to 40%. Projects using FEOC-compliant domestic content equipment add another 10 percentage points, reaching 50%. The low-income community adder adds 10-20 percentage points for qualifying projects, but is subject to allocation limits and not broadly applicable to standard commercial solar.

On a $1.5 million commercial solar project qualifying for the 40% combined credit (base plus energy community), the ITC produces a direct $600,000 reduction in federal tax liability. Combined with MACRS depreciation on the adjusted basis, total first and second year tax benefit often exceeds 55% of original system cost. This is the core of why the ESP zero cap-ex model works — the incentive stack is large enough to fund the system through tax benefit alone.